Reddit: Wall Street Still Doesn't Understand This Business

Q1 2026 EPS came in 3% above Q1 2027 forecast, while consensus 2026 net income just got revised up 16% - and the forecasts are still wrong, particularly on margins

The analyst forecasts are starting to be revised. Consensus net income forecast for 2026 has over the past 3 days been increased from USD 871m to USD 1,014m, a 16% jump. So, even by analyst estimates, Reddit is now trading at 30x forward PE, all the while growing in the sixties %, and with an absolutely clear long-term continuous growth and compounding runway ahead, both from the DAU as well as from ARPU side.

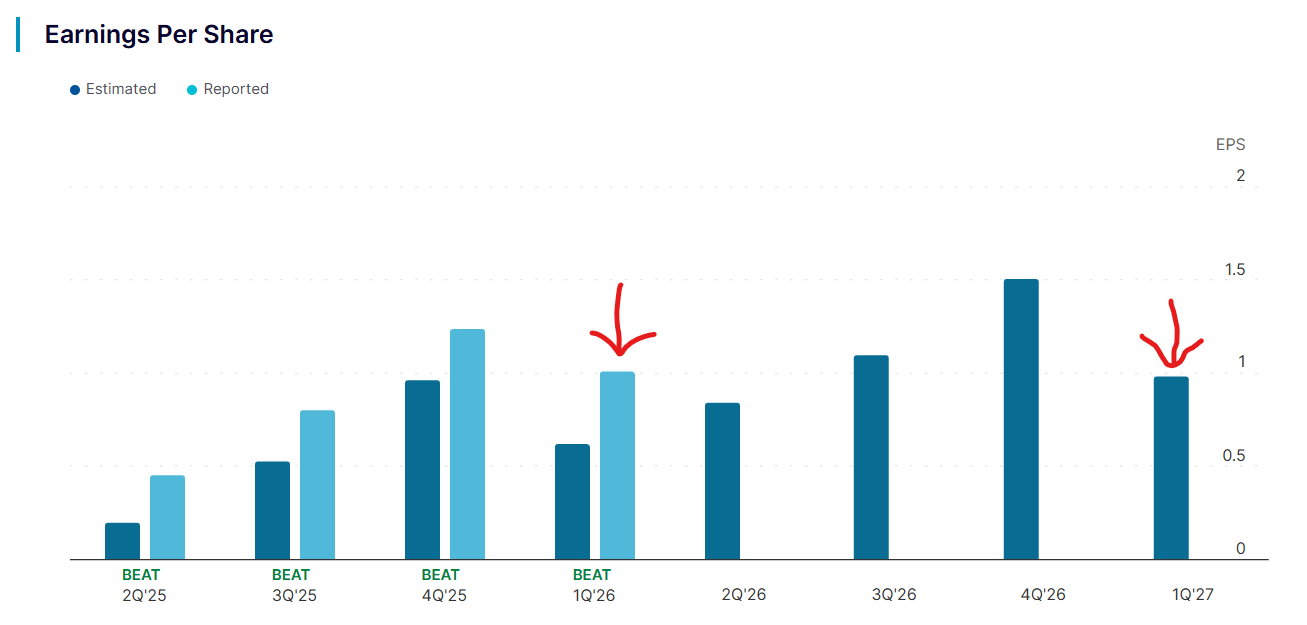

For Q1 2026, Reddit reported 1.01 USD in earnings per share (EPS), which is 61% above analysts’ consensus of 0.62 USD/share, and - even more importantly - is 3% higher than even analyst consensus EPS for Q1 2027, which still stands at 0.98 USD (!). Think about this - Wall Street so fundamentally does not understand Reddit, that its forecast was beaten so hard even their projections for 1 year out on a 60% topline growth business are still lower than the actual numbers already achieved in Q1 2026 - a quarter with no one-offs distorting the numbers. See the chart below for just how consistently Reddit has been obliterating the forecasts, including the comparison of Q1 2026A vs Q1 2027 forecast EPS.

As per above, even with recent revisions, numbers beyond 2026 continue to be disconnected from the underlying reality of Reddit as a business. Reddit is a fabulous business - and it is by far the best business I know of. The platform is largely text based, providing for 91% gross margins. Beyond that, most of the labour is outsourced and provided for free to Reddit, as the moderators are a giant volunteer workforce. The new user acquisition is done “automatically” via a very strong network effect. All that is really needed from the corporate are some fine-tunings to the already existing platform and user experience, but most importantly improvements in monetisation & related continued staffing of ads teams. Finally, capex needs are essentially none - USD 1m in capex for Q1 2026. Thus, Reddit is well positioned to become one of the most profitable companies in the world, with most of the heavy lifting being done by free labour and the network effect. And this is where I believe Wall Street is completely off on Reddit - beyond the also relatively conservative revenue growth projections, see below the development of the net income margin (analyst consensus forecasted numbers are shown for 26-28):

Essentially, analysts are forecasting Reddit’s net income margin, which stood at 35% and 31% in Q4’25 and Q1’26 respectively, to fully stagnate going forward. However, 2025 was the first profitable year for Reddit, meaning only in 2025 did the headline revenues surpass the overhead needed to sustain the website. However, for continued growth in revenues, only minor incremental opex is needed - the fixed costs are already covered with revenues by now. This can also be seen in historical numbers, see below incremental (i.e. current period, less same period 12m ago) revenue and net income development — and importantly, the incremental net income margin.

Incremental net income margin, on the back of the flywheel effect, as of Q1 2026 stood at 65.7%, up from 45.5% in Q2’25. Even assuming this will compress over time, as CIT DTA will expire, adjusting for that we would get to c. 50% incremental net income margins (65.7% margin x (1 – 24% CIT)). This means that net income margin can be expected to continue trending upwards from the current 30% baseline -something completely not captured in analysts’ forecasts, which essentially estimate incremental income margin to start rapidly decreasing down to 35.8% by 2028. Why? The platform is built, the current opex structure calls for 65% pre-tax incremental margins, so a decrease to 35.8% assumes a material decrease in Reddit’s profitability as it scales - an assumption that fundamentally does not make any sense.

Further to the underlying ads business performance - which is the core of the long-term investment thesis, as per outlined in my previous deep dives and my post from 2 weeks ago, there are a number of short to medium term catalysts on the horizon:

The Anthropic lawsuit is so far going heavily in Reddit’s favor. The California district court found that Anthropic was “exploiting Reddit’s platform without authorization and compensation to train and power its AI chatbot Claude, which enriched Anthropic by billions of dollars. These elements are qualitatively different from a copyright claim.” This distinction matters, as AI companies defending against content scraping lawsuits have consistently relied on fair use - a doctrine under US copyright law that, under certain conditions, allows using protected content without permission. While a strong shield, it only works as a defense to copyright claims. On the contrary, Reddit is suing over Anthropic breaking its Terms of Service. By ruling that Reddit’s claims are qualitatively different from copyright infringement, the court effectively removes Anthropic’s most powerful defense. You can’t fair use your way out of a contract breach. With Anthropic’s planned IPO on the horizon, a settlement seems like the most likely outcome - they likely won’t want a major lawsuit overhang while going public. Either way, a large one-off settlement plus a licensing agreement looks very probable. Importantly, at current valuations, and as per my deep dive, you are paying nothing for this upside - it’s a pure free option. At the same time, this might be a catalyst for the market’s view on licensing income to change - if Anthropic has to start paying USD X00m annually for licensing, this flows directly to the bottom line (tax is the only expense). This is essentially a 100% pre-tax margin, stable & with positive outlook revenue stream.

The above also sets a strong precedent for the pending Perplexity lawsuit, as well as upcoming & already underway Google & OpenAI licensing deals re-negotiations, the existing contracts with both set to expire in Q1–Q2 2027

With all S&P 500 inclusion criteria are still being met, hence index inclusion remains a short-to-medium term catalyst - which historically brings meaningful passive buying pressure

Similar to Meta, Reddit should be one of the key beneficiaries of the AI boom, as improved AI can be used to further improve the monetisation of users / ad targeting under an expedited timeline and with minimal incremental costs. And while Meta’s platforms are already heavily optimised, meaning any incremental targeting improvement requires relatively heavier investment (see their surging capex commitments for compute), Reddit is still very early in the monetisation journey, hence should have a lot of low hanging fruit left to pick, before incremental improvements start becoming challenging. To this end, Reddit carries minimal AI downside (as capex is essentially zero), but large upside as the targeting should continue improving

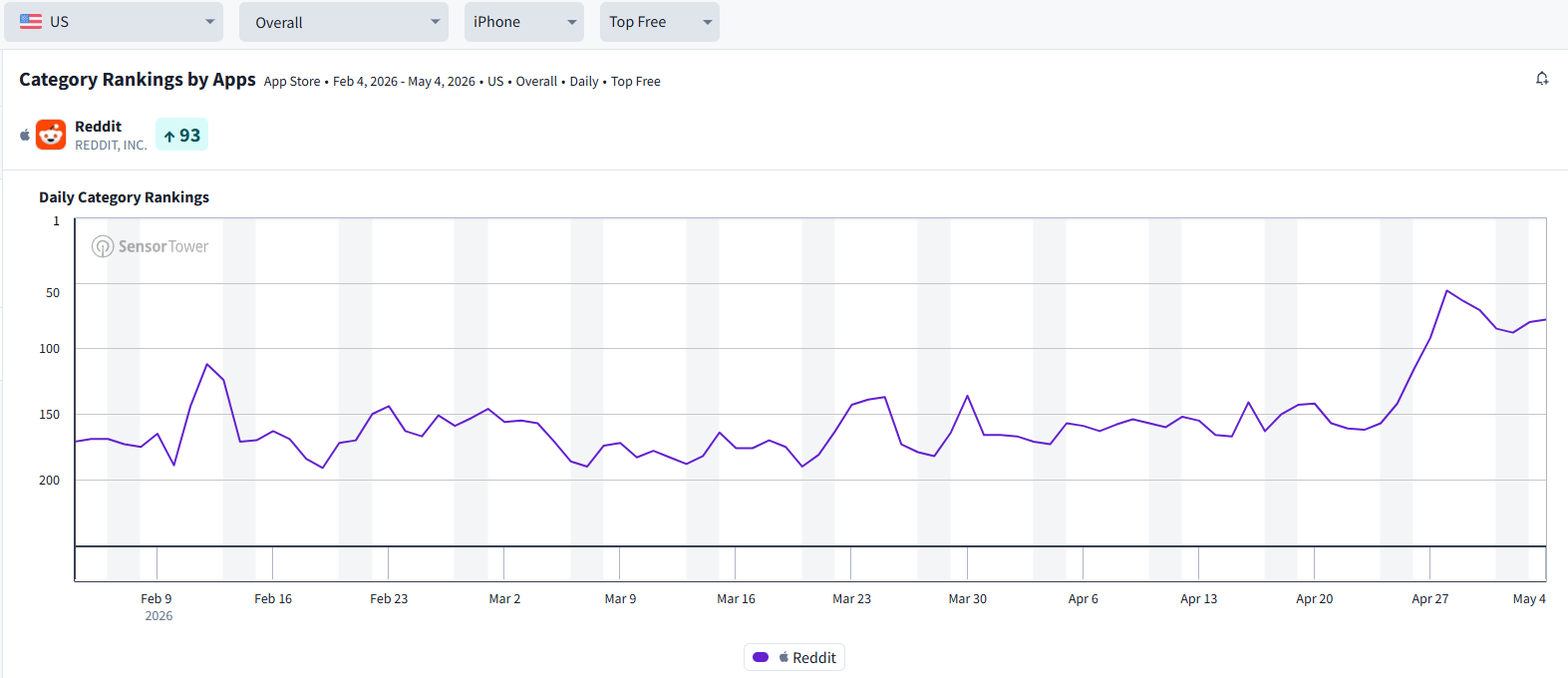

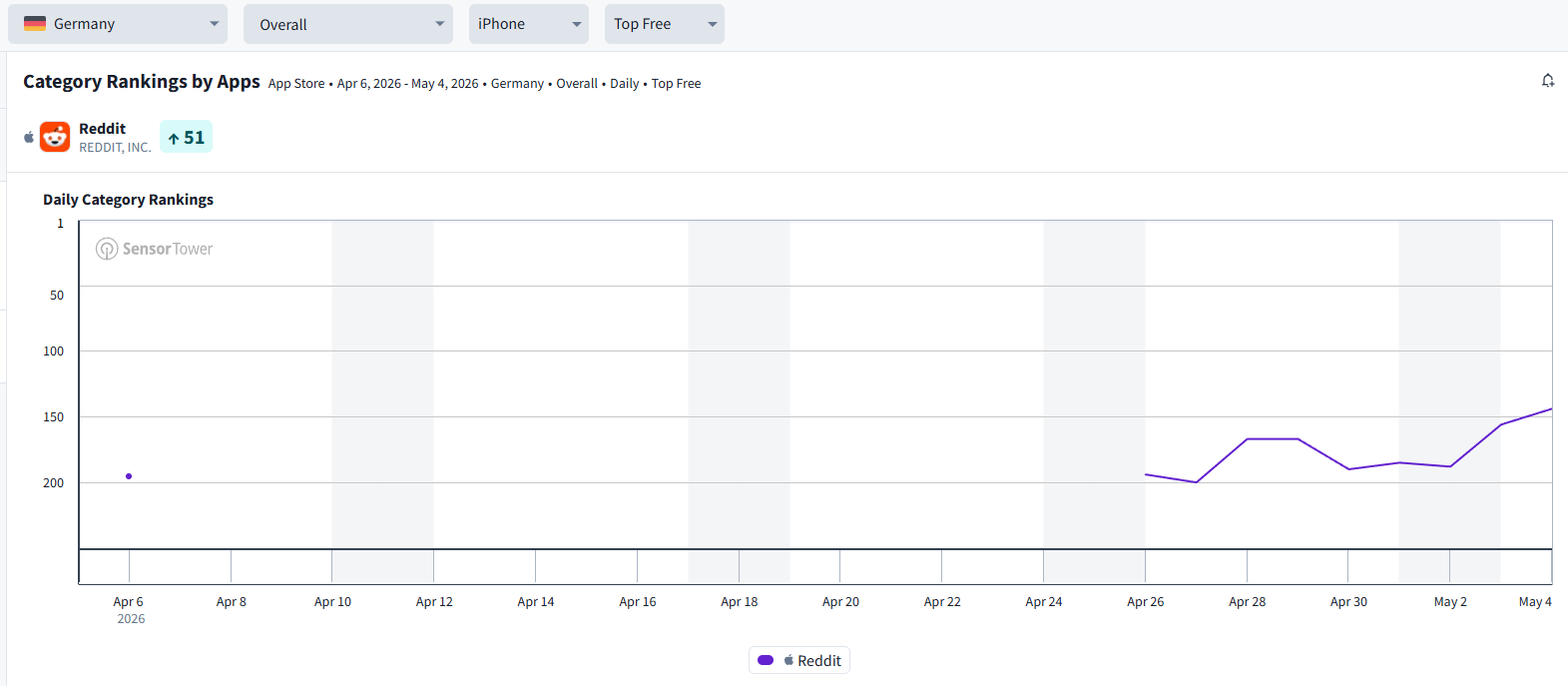

US DAUq stagnation scare might be coming to an end - users have been reporting pop-ups to install the app, if they visit Reddit outside the mobile app. This should naturally increase the app downloads and thus logged-in users growth. We can already start seeing the effect in iOS App Store downloads trackers - Reddit jumped from position #162 to #78 in the US over the past 2 weeks. Similar trend can be seen also in UK (from #180 to #85) and Germany (from #194 to #144).

To this end, it appears we are likely to see a “positive surprise” on logged-in DAUq user growth for Q2 2026 earnings - which will also be the last quarter in which Reddit will report this split (they announced starting Q3 this year the split between logged-in and logged-out users will no longer be reported). That’s a good strategy - ensure a positive development and surprise just before the end of reporting of a metric.